IPO Analysis of PT Dayamitra Telekomunikasi Tbk

ALI ABDILAHI

ALI ABDILAHI

2602650914 · Business School

Corporate Finance · IPO Analysis

PT DAYAMITRA TELEKOMUNIKASI TBK (MTEL — Mitratel)

IPO Analysis: Great Company, Great Execution — But Was the Price Right?

IPO Date: November 22, 2021 · Ticker: MTEL · Indonesia Stock Exchange (IDX)

SECTION I

IPO Overview & Offering Structure

The Offering

PT Dayamitra Telekomunikasi Tbk (‘Mitratel’) is a subsidiary of PT Telkom Indonesia that leases telecommunication towers. It went public via an Initial Public Offering (IPO) on November 22, 2021. During this IPO, the Company offered 22,920,512,000 newly issued ordinary shares — comprising 27.63% of issued and paid-up capital after the close of the Offering — at a price of IDR 800 per share (par value IDR 228), representing an aggregate offering value of IDR 18,336,409,600,000 (approximately IDR 18.34 trillion).

In the event of oversubscription through centralised allotment, the Company retained the right to issue up to an additional 2,619,487,000 shares (up to 3.06% of post-IPO capital), bringing the maximum total offering to 25,539,999,000 shares (maximum value IDR 20.43 trillion). The Offering Period ran from November 16–18, 2021, with shares listed on the IDX on November 22, 2021.

Emission Cost Breakdown

SECTION II

IPO Objectives & Use of Proceeds

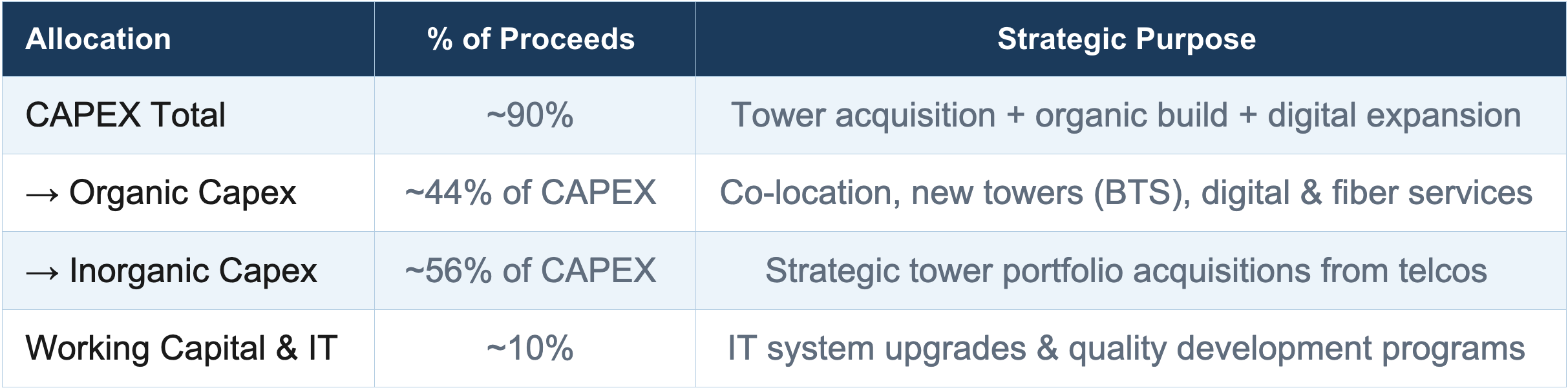

Proceeds Allocation

Per Chapter II of the Prospectus (Rencana Penggunaan Dana), the Company intended to use all net proceeds after deducting emission costs as follows: approximately 90% allocated to capital expenditure (belanja modal), split ~44% organic capex and ~56% inorganic capex; with the remaining ~10% directed to working capital and IT upgrades.

Evaluation: Are IPO Objectives Being Met?

Overall, there is clear evidence that Mitratel has remained true to its IPO objectives, exhibiting significant discipline in strategic execution. The company’s financial results from 2021 through 2025 confirm that every major allocation was delivered.

Inorganic Capex: Acquisitions Delivered at Scale

The largest allocation — inorganic capex — was executed with landmark precision. In 2022, Mitratel acquired 6,000 towers from Telkomsel, placing it as Southeast Asia’s largest tower operator. This was followed in Q1 2023 by an additional acquisition of 997 towers from Indosat Ooredoo Hutchison (IOH), representing IDR 2.17 trillion in investing cash flows for the quarter. The company grew from 28,206 to 39,404 towers from 2021 to end-2024 — a 40% growth rate, predominantly driven by inorganic acquisitions precisely as outlined in the prospectus.

Organic Capex: New Towers & Fiber Expansion

Organic allocation was also actively deployed. Capital expenditures through organic capex spending were IDR 2.88 trillion in 2024 and IDR 2.18 trillion in 2025, consistent with historical annual capital expenditure levels. The fiber optic network expanded from virtually nothing prior to IPO to 51,039 kilometres as of December 31, 2024 — directly aligned with the objective of diversifying into digital and fiber services. The fiber and tower segments collectively generated revenues of IDR 8.67 trillion in 2024.

SECTION III

Post-IPO Financial Performance (2021–2025)

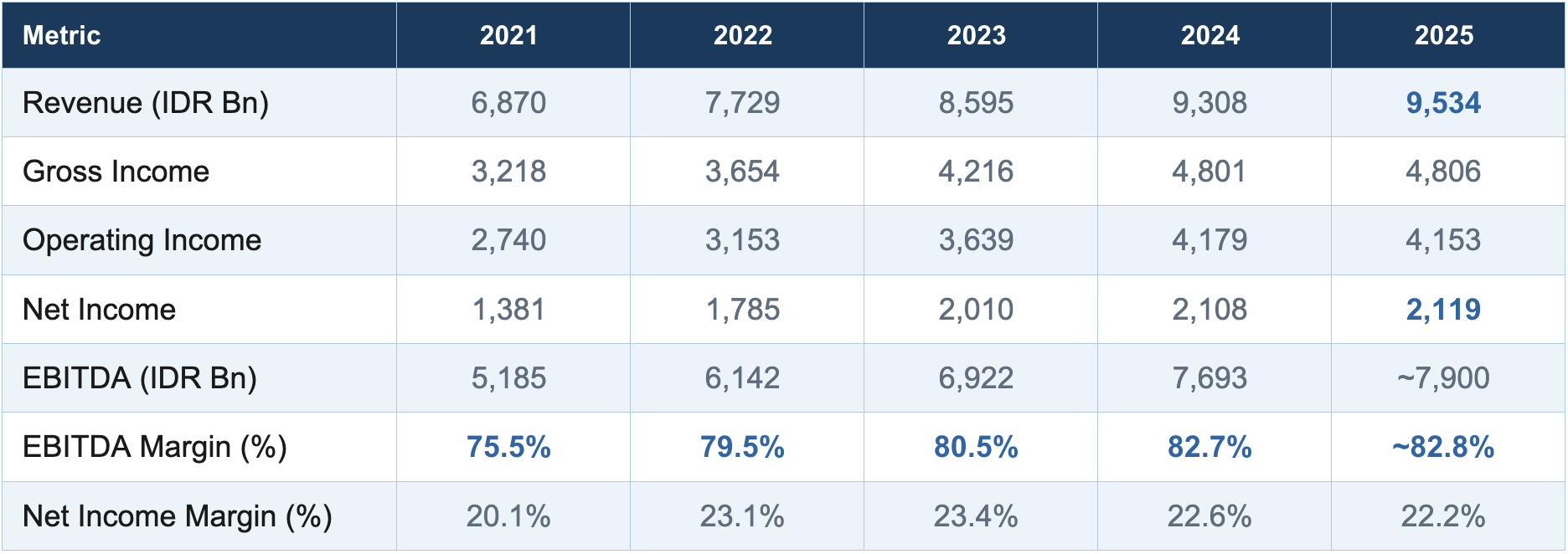

Mitratel’s five-year post-IPO financial track record demonstrates consistent and strengthening performance across all key metrics, validating the company’s growth strategy. Revenue has grown uninterrupted every year since listing, and EBITDA margins have consistently expanded — reflecting the operating leverage inherent in tower infrastructure as colocation density increases.

Income Statement Summary (IDR Billion)

Revenue grew from IDR 6.87 trillion (FY2021) to IDR 9.53 trillion (FY2025) — a cumulative growth of 38.7% over four years. Net income more than doubled from IDR 1.38 trillion to IDR 2.12 trillion, growing at a compound rate of approximately 11% per year. Crucially, EBITDA margin expanded from 75.5% to over 82.8%, reflecting economies of scale from in-market tower acquisitions generating new colocation revenues at low incremental costs.

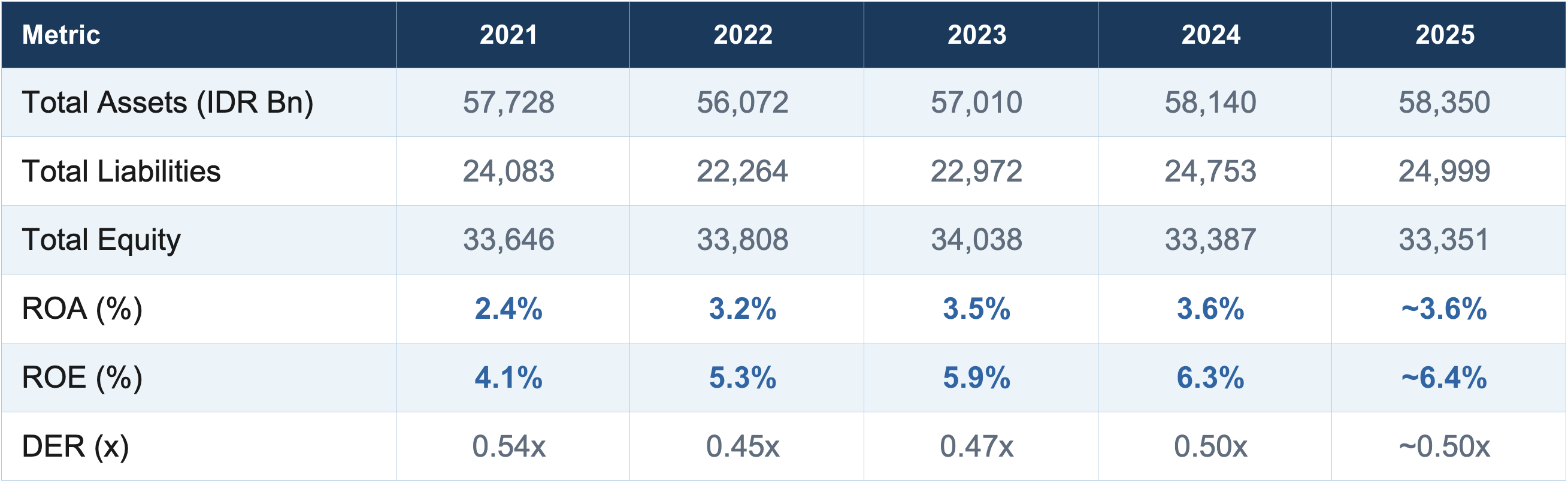

Balance Sheet & Returns (IDR Billion)

Total assets stabilised around IDR 57–58 trillion after the post-IPO cash deployment peak. Return on equity improved from 4.1% in 2021 to 6.3% in 2024, reflecting more efficient utilisation of the enlarged equity base. The debt-to-equity ratio improved from 0.54x at IPO to a stable 0.45–0.50x range — demonstrating disciplined leverage management despite significant acquisition activity.

Cash declined from IDR 19.1 trillion at IPO to IDR 609 billion at year-end 2025, reflecting the systematic and purposeful deployment of IPO proceeds. Long-term loans increased to IDR 15.25 trillion, but net debt to EBITDA remained disciplined at approximately 1.4–2.3x — within manageable ranges for a capital-intensive infrastructure business.

SECTION IV

Post-IPO Stock Price Performance

Initial Momentum & 2022 Volatility

On November 22, 2021, PT Dayamitra Telekomunikasi Tbk (MTEL) went public on the Indonesia Stock Exchange at an IPO price of IDR 800 per share. Following the listing, the stock showed good momentum and reached a high of IDR 835 before closing at IDR 830 by end-Q4 2021 — demonstrating positive early demand for this new tower infrastructure company.

Post IPO Stoke Performance

MTEL Stock Price & Volume (Nov 2021 – Dec 2022). Source: PT Dayamitra Telekomunikasi Tbk Annual Report 2022

MTEL Stock Price & Volume (Nov 2021 – Dec 2022). Source: PT Dayamitra Telekomunikasi Tbk Annual Report 2022

By end-2022, however, the stock began showing signs of gradual decline. In Q1 2022, MTEL closed at IDR 770 and continued declining in Q2 to IDR 700 — the lowest level of the study period. Multiple factors drove this: weakness in global financial markets and rising interest rate concerns affecting infrastructure company valuations globally. In Q3 2022 the stock recovered incrementally to IDR 725, and by Q4 2022 had bounced back to its IPO price of IDR 800. Throughout 2022, even when pricing was weak mid-year, the stock maintained a large market cap of IDR 58.5–66.8 trillion, driven by the company’s operational success with full-year revenue growth of 12.51% and net income growth of 29.25%.

Medium-Term Drift Below IPO Price

Despite stellar operational performance, as of 2024 the company’s stock was trading below its IDR 800 IPO price. After reaching IDR 640 in mid-2022 and drifting down to IDR 615 by 2024, investors who held for three years found that inflation had eroded their purchasing power while sitting on a nominal loss. This illustrates a fundamental principle of IPO investing: a great company is not always a great stock at the IPO price.

SECTION V

Investment Decision Analysis

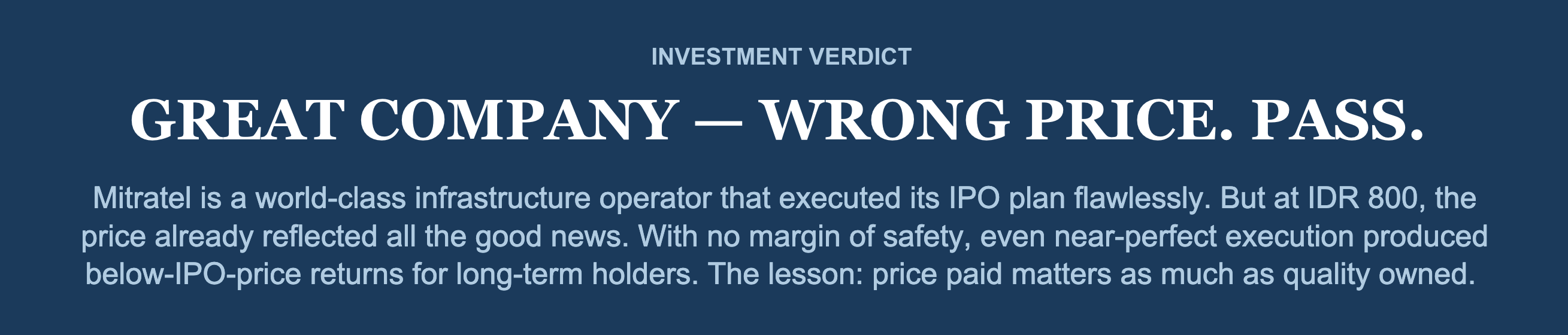

The Counterintuitive Verdict: Pass

Would I invest in Mitratel at IPO? No — and here is why that is actually the highest compliment I can pay to rigorous investment analysis. There is no denying that Mitratel is an outstanding company. Its performance has been stellar: tower count grew from 28,206 to over 39,000; revenues expanded from IDR 6.87 trillion to IDR 9.53 trillion in 2025; EBITDA margins increased from 75.5% to over 82%; and management delivered almost exactly what it promised in the prospectus — including the historic acquisition of 6,000 towers through Telkomsel to become Southeast Asia’s largest tower company. Impressive? Unquestionably.

Great Company. Wrong Price.

But here is the harsh reality: despite near-perfect execution, as of 2024 the stock was trading below its IDR 800 IPO price. This is the cardinal sin of IPO investing — confusing a great company with a great price at which to buy that company’s stock. At IDR 800, Mitratel was sold at a price that already assumed its great qualities had been factored in. When you pay ‘full price’ for a premium-quality company, there is absolutely no margin for error and no upside left — even when everything goes right operationally.

The stock’s trajectory confirms this: despite 39% revenue growth, 53% net income growth, and EBITDA margins consistently above 79%, the stock underperformed its IPO price for years. This is not a failure of the business — it is a failure of the entry price. The investment framework is simple: great company + fair price = good investment; great company + full price = poor investment. Mitratel at IPO was the latter.

SECTION VI

SECTION VI

Conclusion

Following a comprehensive analysis of the IPO and post-IPO performance of PT Dayamitra Telekomunikasi Tbk, it is clear that Mitratel’s 2021 IPO was an exceptional exercise in capital deployment and strategic execution. The company raised IDR 18.34 trillion, allocated it precisely as outlined in the prospectus — 90% to capex split between organic and inorganic growth — and delivered results that met or exceeded every stated objective.

The operational outcomes are remarkable: tower count grew 40% to 39,404; fiber optic network expanded to 51,039 kilometres; revenue grew 38.7% over four years; net income nearly doubled; and EBITDA margins expanded from 75.5% to over 82.8%. Mitratel is now the largest independent tower operator in Southeast Asia — a transformation from a single-operator subsidiary to a regional infrastructure champion, accomplished in under four years.

Yet the investment verdict is clear: the stock underperformed its IPO price for years despite this stellar operational performance — a direct consequence of IPO pricing that left no margin of safety for investors. The lesson is enduring: in IPO investing, the quality of the business and the quality of the entry price are entirely separate questions. Mitratel answers the first question with an unequivocal A+. At IDR 800, it answers the second with a different conclusion. Great company. Wrong price. My money stays in my pocket.

REFERENCES

Sources & Bibliography

- PTDayamitraTelekomunikasi Tbk. (2021). Laporan Tahunan 2021 (Annual Report). https://www.mitratel.co.id/annual-report/

- PTDayamitraTelekomunikasi Tbk. (2022). Laporan Tahunan 2022 (Annual Report). https://www.mitratel.co.id/annual-report/

- PTDayamitraTelekomunikasi Tbk. (2023). Laporan Tahunan 2023 (Annual Report). https://www.mitratel.co.id/annual-report/

- PTDayamitraTelekomunikasi Tbk. (2024). Laporan Tahunan 2024 (Annual Report). https://www.mitratel.co.id/annual-report/

- PTDayamitraTelekomunikasi Tbk. (2026). Financial Statements 2025. https://www.mitratel.co.id/wp-content/uploads/2026/04/dayamitra-telekomunikasi-tbk-bilingual_31-desember-2025_released.pdf

- PTDayamitraTelekomunikasi Tbk. (2023). Info Memo Q1 2023. https://www.mitratel.co.id/wp-content/uploads/2023/05/MTEL-Info-Memo-1Q-2023_Indo.pdf

- PTDayamitraTelekomunikasi Tbk. (2021). Prospektus Penawaran Umum Perdana Saham (IPO Prospectus). https://e-ipo.co.id/id/ipo/52/mtel-pt-dayamitra-telekomunikasi-tbk

YOUR NEXT STEP

Join MM Pro

Binus Business School

Be Part of a Global Academic Community

Sharpen your business acumen, expand your global network, and lead with confidence in the world’s most dynamic markets.

Comments :