Indonesia’s Green Giant: Did PGEO’s Rp9 Trillion IPO Deliver?

PT Pertamina Geothermal Energy Tbk listed in February 2023 as one of Indonesia’s largest renewable energy IPOs. Three years on, its balance sheet is stronger — but operational efficiency is under serious pressure.

Rivano Naufal Nugroho

Rivano Naufal Nugroho

MBA Candidate · Binus Business School · Student ID: 2602659011

Individual Paper for Corporate Finance · May 2026 · 13 min read

The global push toward Net Zero Emissions has made the renewable energy sector a national priority — and Indonesia, holding approximately 40% of the world’s geothermal reserves, sits in a uniquely powerful position to lead that transition. When PT Pertamina Geothermal Energy Tbk (PGEO) listed on the Indonesia Stock Exchange on February 24, 2023, it wasn’t just a corporate event. It was a statement of national ambition.

At an IPO price of Rp875 per share across 10.35 billion new shares, PGEO raised approximately Rp9.05 trillion — one of the largest IPOs in Indonesia’s renewable energy sector. The mandate was clear: use the capital to restructure the balance sheet, fund massive capacity expansion, and position the company as the country’s premier pure-play geothermal entity.

Three years on, this article provides a rigorous assessment of whether that mandate has been fulfilled. Drawing on the company’s IPO prospectus, financial statements through 2025, and market data, we examine the IPO objectives, the deployment of proceeds, post-IPO financial performance, stock price dynamics, and what investors should make of the company today.

1. Company Overview

PT Pertamina Geothermal Energy Tbk is a subsidiary of PT Pertamina (Persero), Indonesia’s state-owned oil and gas giant, tasked with managing the country’s Geothermal Working Areas (WKP). As the largest pure-play geothermal company in Indonesia — and one of the largest in the world — PGEO operates across the full value chain from upstream exploration to downstream electricity generation.

The company’s operational footprint spans multiple strategic WKPs across Sumatra and Java, including the Lumut Balai, Hululais, and Gunung Way Panas areas. Its status as a state enterprise affiliate gives it privileged access to geothermal concessions and strong regulatory support — a structural competitive advantage that few private entrants can replicate.

From an ownership perspective, PGEO’s concentrated shareholding structure — with Pertamina Power Indonesia as the dominant anchor — provides strategic stability while public ownership enhances market liquidity. This combination of state backing and public accountability makes PGEO a distinctive instrument in Indonesia’s capital markets.

2. IPO Objectives & Proceeds

PGEO’s February 2023 IPO involved the issuance of 10,350,000,000 new shares at Rp875 each, generating gross proceeds of Rp9,056,250,000,000 — approximately Rp9.05 trillion. Net proceeds, after deducting underwriting fees, professional support costs, and listing administration charges, were allocated across two primary strategic pillars: capital expenditure expansion and financial liability restructuring.

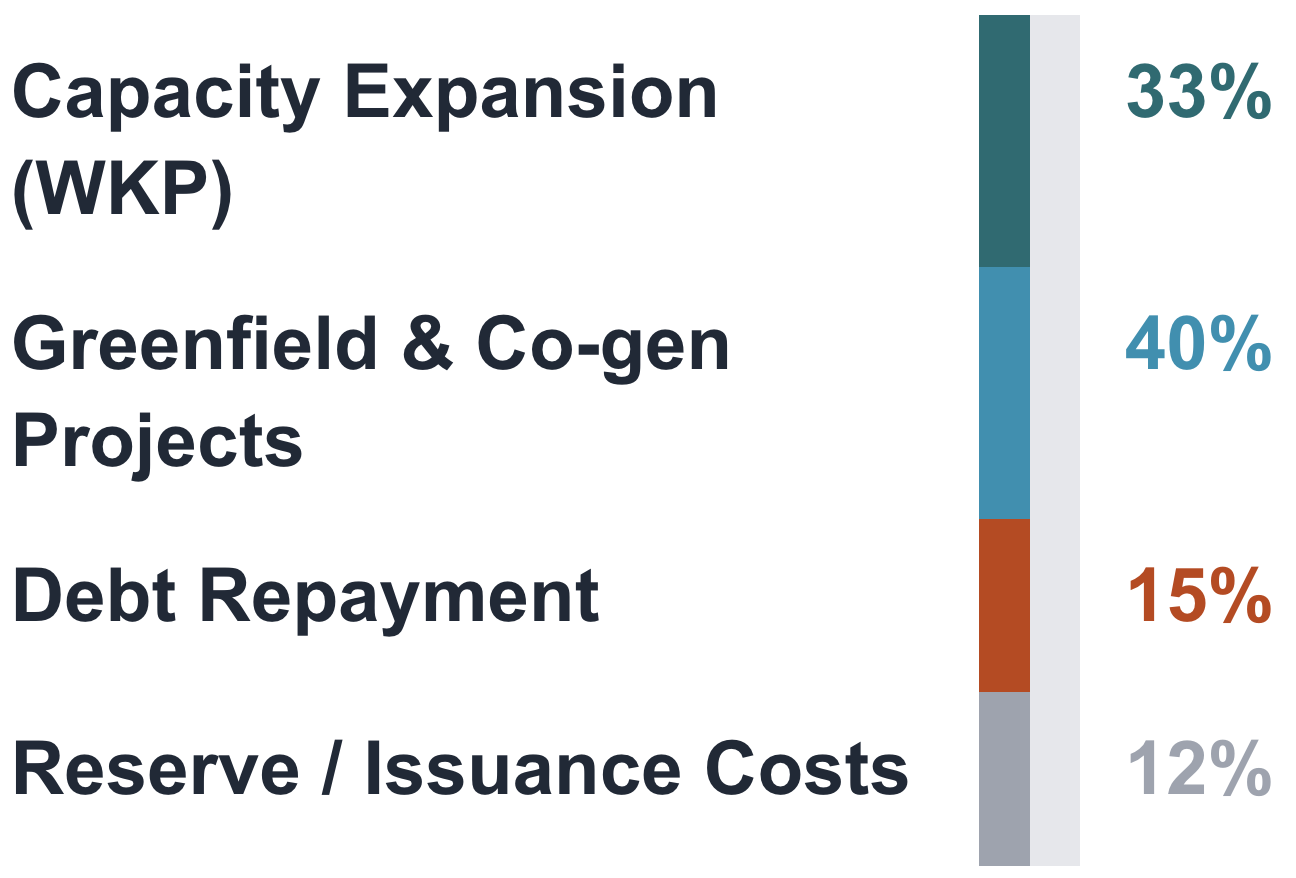

Figure 1 · PGEO Net IPO Proceeds Allocation (Source: PGEO IPO Prospectus, 2023)

Figure 1 · PGEO Net IPO Proceeds Allocation (Source: PGEO IPO Prospectus, 2023)

Capital Expenditure — 85% of Net Proceeds

The dominant allocation — roughly 85% of net proceeds — was designated for physical infrastructure expansion across two categories. Approximately 33% was directed toward developing additional capacity in existing WKPs such as Lumut Balai, Hululais, and Gunung Way Panas, where existing infrastructure could be leveraged to accelerate output. The remaining 40% targeted greenfield project development and co-generation technology implementation to improve geothermal steam efficiency — a technically complex but high-reward undertaking that underpins the company’s long-term 1 GW installed capacity ambition.

Debt Repayment — 15% of Net Proceeds

The remaining 15% of net proceeds was specifically allocated to repaying obligations under the Facilities Agreement dated June 23, 2021 with an international banking syndicate. The strategic rationale was to immediately reduce the company’s Weighted Average Cost of Capital (WACC), strengthen net profit margins, and give management greater financial flexibility to navigate the volatile macroeconomic environment post-listing.

3. Evaluation of Proceeds Utilisation

Evaluating the post-IPO fund realization reveals a clear asymmetry: the financial restructuring component was executed swiftly, while the physical capital expenditure absorption has proceeded far more gradually.

The 15% debt repayment allocation was fully realized within months of the IPO listing. This rapid execution delivered an immediate improvement in the company’s solvency ratios and eliminated the burden of ongoing interest costs under the original Facilities Agreement — a clear win for balance sheet management.

In contrast, the 85% CAPEX allocation for upstream infrastructure development has followed a much slower absorption curve. Geothermal project development is inherently sequential and technically demanding: drilling activities carry significant failure probabilities, land permits require extended regulatory coordination, and supporting infrastructure must be ready before new wells can contribute to the energy grid. These are not execution failures — they are structural characteristics of the industry.

During the extended waiting period, management placed idle IPO funds in time deposit instruments at national banks — a capital preservation strategy that generated meaningful interest income in the first post-IPO fiscal year. While this approach was prudent from a liquidity standpoint, sustained reliance on non-operating income to support net profit figures has drawn scrutiny from market analysts who argue that capital should be converted into productive energy assets more rapidly.

To accelerate fund absorption, PGEO is actively developing strategic cooperation schemes with global and domestic technology partners. These partnerships aim to share the burden of high-risk upstream drilling while accelerating the deployment of reservoir processing innovations at Lumut Balai and Hululais.

4. Post-IPO Financial Performance

Revenue Trajectory

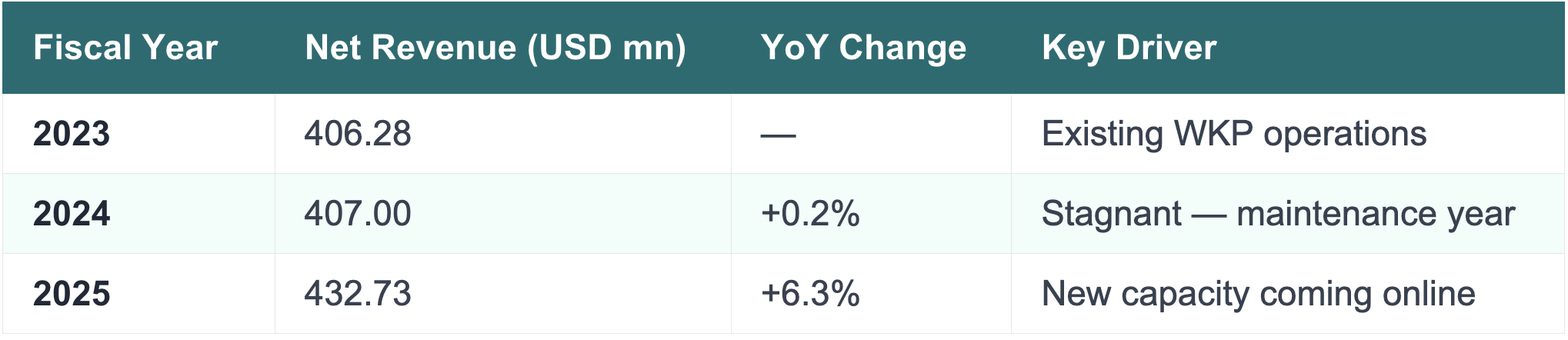

Table 1 · PGEO Revenue Performance, 2023–2025 (Sources: PGEO Financial Statements 2023–2025)

Table 1 · PGEO Revenue Performance, 2023–2025 (Sources: PGEO Financial Statements 2023–2025)

Revenue performance post-IPO shows a moderate but increasingly encouraging growth trajectory. After virtual stagnation between 2023 and 2024 (with revenue essentially flat at USD 406–407 million), the 2025 fiscal year saw a meaningful 6.3% acceleration to USD 432.73 million. This uptick directly reflects the first commercial contributions from IPO-funded upstream infrastructure — early validation that the capital expenditure strategy is beginning to deliver commercial output.

Net Income: The Pressure Point

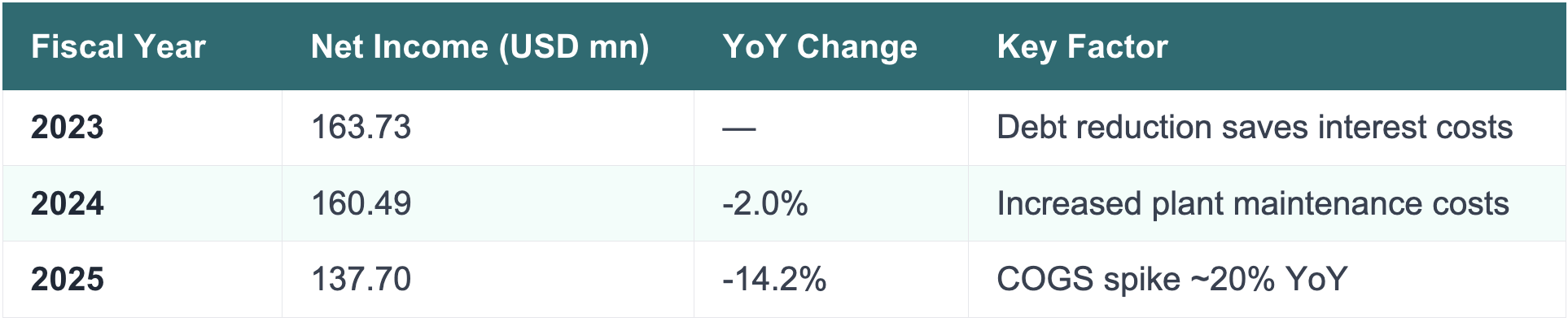

Table 2 · PGEO Net Income Performance, 2023–2025 (Sources: PGEO Financial Statements; SWA, 2026)

Table 2 · PGEO Net Income Performance, 2023–2025 (Sources: PGEO Financial Statements; SWA, 2026)

While revenue has grown, net income tells a more complicated story. The 2023 surge to USD 163.73 million was largely driven by the one-time benefit of debt repayment — interest expenses dropped dramatically, boosting the bottom line. That tailwind moderated in 2024 to USD 160.49 million as maintenance costs on ageing plant infrastructure increased.

The 2025 result is the most concerning: net income fell 14.2% to USD 137.7 million despite revenue growth. The culprit was a nearly 20% spike in Cost of Goods Sold (COGS), driven by intensified maintenance schedules, drilling cost escalation, and operational inefficiencies across power plant areas. This cost surge eroded profitability even as electricity sales volumes expanded — a critical signal that operational cost management must become management’s top priority in the near term.

Balance Sheet & Liquidity

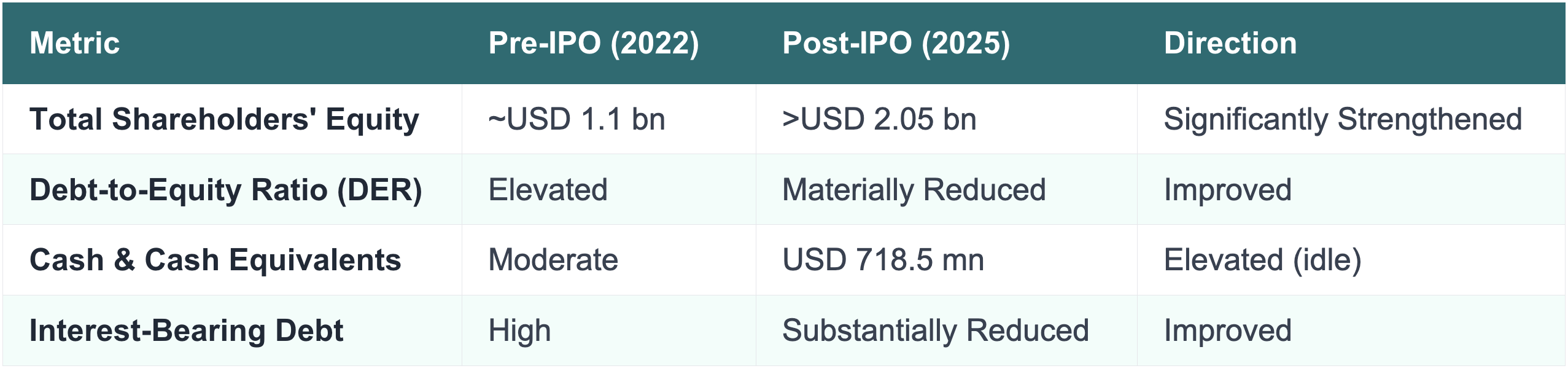

Table 3 · Balance Sheet Transformation, Pre- vs. Post-IPO (Sources: PGEO Financial Statements 2025)

Table 3 · Balance Sheet Transformation, Pre- vs. Post-IPO (Sources: PGEO Financial Statements 2025)

The IPO has fundamentally transformed PGEO’s financial risk profile. Shareholders’ equity has grown to over USD 2.05 billion by end-2025, the direct result of both the IPO equity infusion and accumulated post-IPO earnings. The Debt-to-Equity Ratio improved dramatically following the 15% proceeds debt repayment, giving management significantly more financial flexibility.

However, the USD 718.5 million cash balance — while reflecting the company’s immense liquidity — also signals the slow pace of CAPEX absorption. Large idle cash balances generated valuable time deposit interest income in 2023, but analysts increasingly view this as a sub-optimal use of shareholders’ capital that must be resolved through accelerated infrastructure deployment.

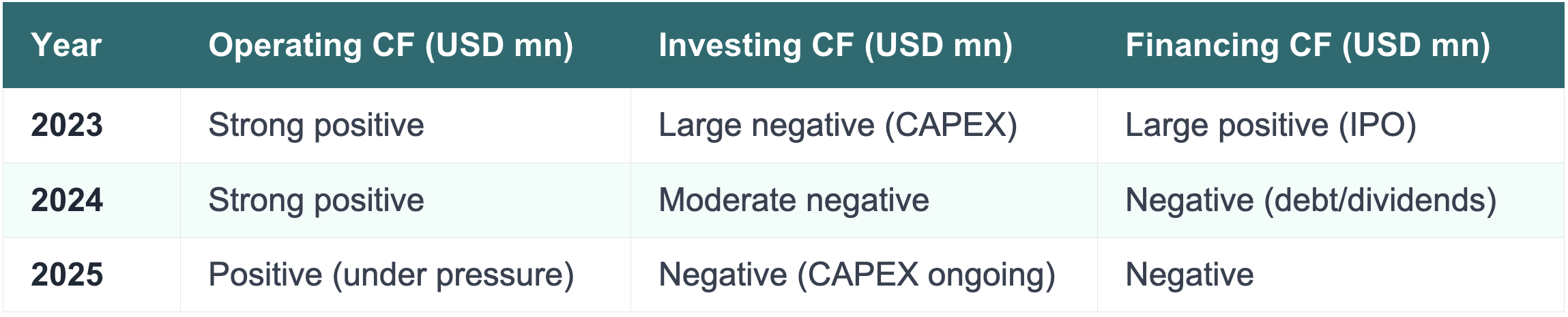

Cash Flow Quality

Table 4 · Cash Flow Summary, 2023–2025 (Source: PGEO Financial Statements)

Table 4 · Cash Flow Summary, 2023–2025 (Source: PGEO Financial Statements)

Operating cash flow has remained positive throughout the post-IPO period, even as net income came under pressure in 2025 — a reassuring indicator that the business continues to generate real cash from operations. The large negative investing cash flows reflect ongoing capital expenditure commitments, which confirms that CAPEX deployment, while slower than prospectus timelines, is actively progressing.

5. Stock Price Movements & Market Response

PGEO’s stock market journey since its February 2023 listing has been a textbook case of the tension between strategic ambition and investor impatience in a capital-intensive sector.

Phase 1: Cautious Reception (Early 2023)

Despite PGEO’s status as the largest renewable energy issuer on the IDX, the opening trading period showed moderate volatility with a tendency to drift below the Rp875 IPO price. Market participants appeared cautious — the geothermal business model requires a long investment horizon before demonstrating real production capacity growth, and in a period of broader macroeconomic uncertainty, many investors priced in that risk premium immediately.

Within the first six months, the stock briefly entered sub-IPO-price territory, triggering institutional skepticism. The low initial CAPEX absorption rate — funds sitting in time deposits rather than converting to installed capacity — was cited by analysts as a key reason for the muted institutional appetite.

Phase 2: Gradual Recovery (2024)

As 2024 progressed, transparency in operational disclosures and the publication of concrete progress toward the 1 GW capacity target began to rebuild investor confidence. The release of solid 2024 full-year financial results provided a positive catalyst. Market analysts began drawing connections between the government’s energy transition commitments and the long-term sustainability of PGEO’s cash flow model, gradually shifting the narrative from skepticism to recognition of intrinsic value.

Phase 3: Resilience & Upside Potential (2024–2026)

PGEO has demonstrated notable resilience during periods of global geopolitical turbulence. The 2024 Iran-Israel conflict escalation, which rattled many asset classes, did not significantly impact PGEO’s stock — a finding that reinforces the investment thesis of geothermal energy as a defensive, ESG-compliant asset that is largely decoupled from crude oil price swings.

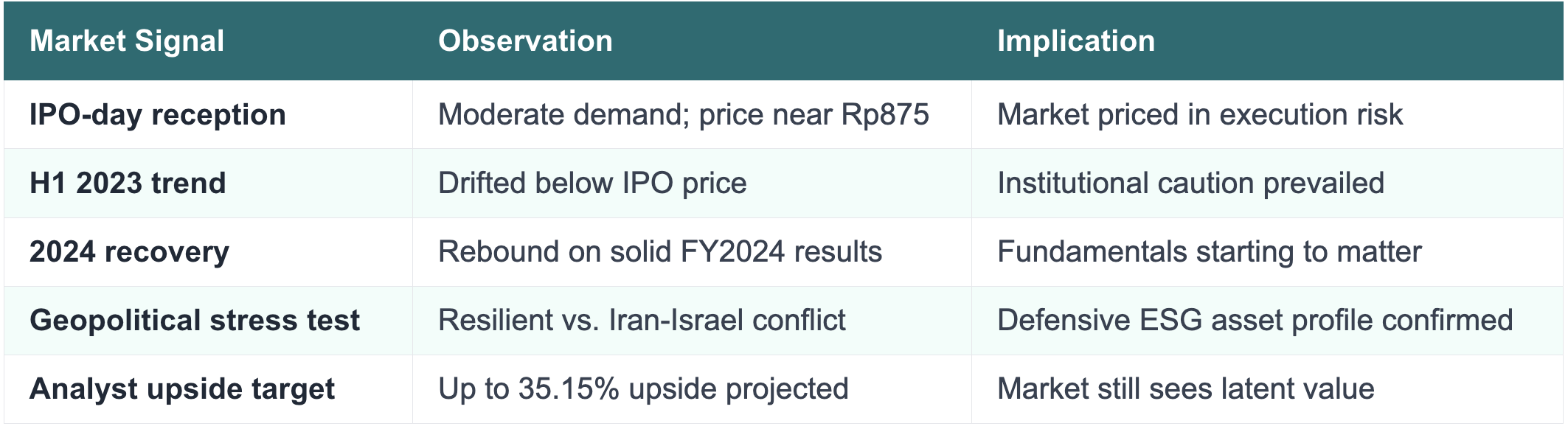

Table 5 · PGEO Market Signal Summary (Sources: Yahoo Finance; Bloomberg Technoz; Investor Trust, 2024–2025)

Table 5 · PGEO Market Signal Summary (Sources: Yahoo Finance; Bloomberg Technoz; Investor Trust, 2024–2025)

Market research projections of up to 35.15% upside potential signal that analysts remain constructive on PGEO’s long-term value — particularly as new geothermal working areas begin contributing commercial output and as strategic technology partnerships accelerate cost efficiency. However, the 2025 earnings miss has introduced caution: the market will need to see demonstrated improvement in COGS management before consensus upgrades fully materialise.

6. Decision Analysis: Should You Have Invested?

Assessing the investment case for PGEO at its Rp875 IPO price requires separating two distinct questions: Was the underlying business worth buying? And was the stock’s short-term trading behaviour predictable? The answers diverge significantly.

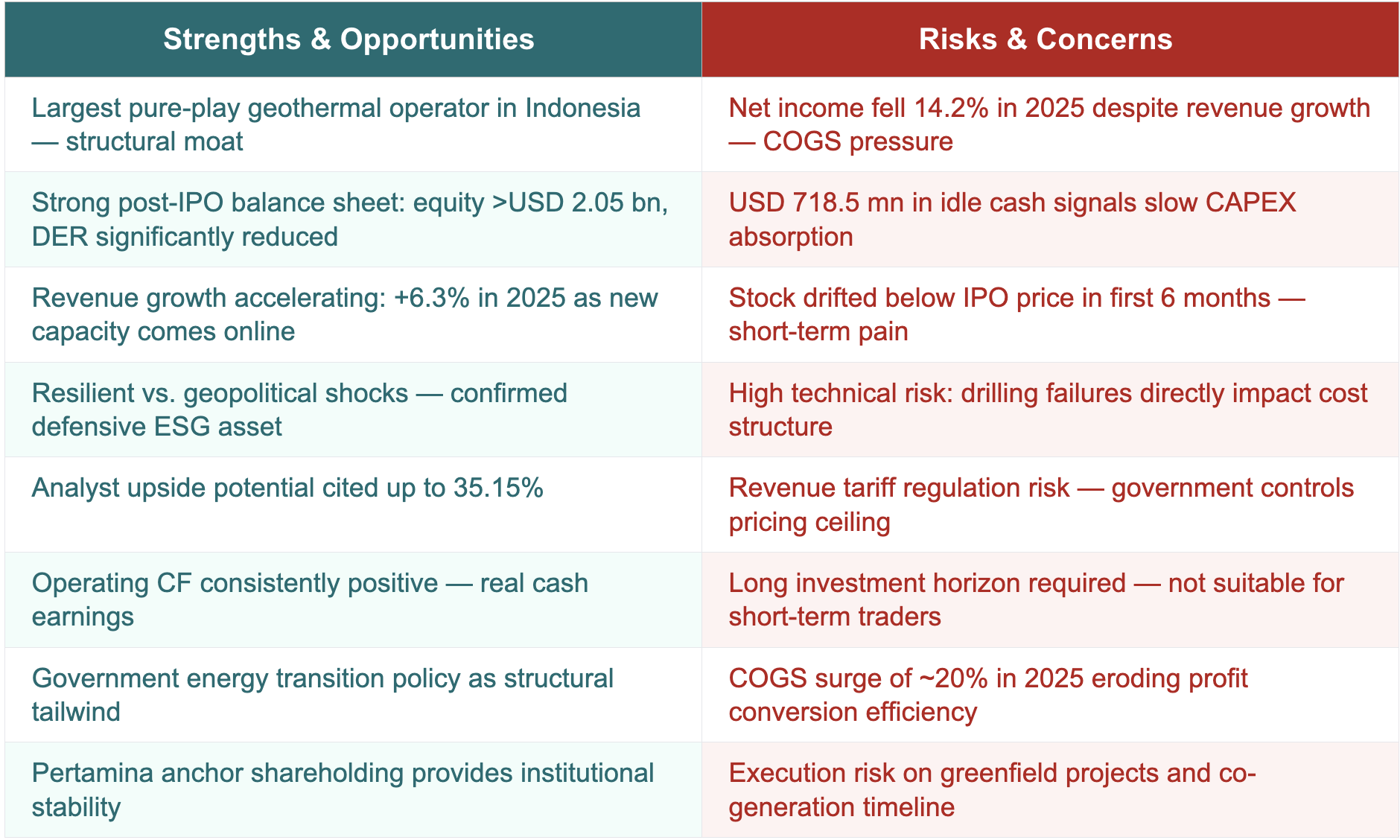

From a fundamental standpoint, the IPO decision was rational for patient investors. The immediate balance sheet improvement — debt repayment funded by 15% of IPO proceeds — was a near-certain positive outcome. The strategic positioning of PGEO as Indonesia’s dominant geothermal operator, backed by Pertamina’s institutional weight and government energy policy tailwinds, represented genuine long-term value.

For short-term investors, the early months of PGEO’s listing were genuinely difficult. The stock’s lethargic price behaviour, sub-IPO-price trading, and slow CAPEX absorption provided little short-term fuel. An investor expecting instant post-IPO gains would have been disappointed.

For long-term investors with an ESG mandate and a three-to-five year horizon, the fundamental case remains compelling. The 2025 net income pressure — while real — is primarily a COGS management challenge rather than a structural business model failure. Revenue is growing. Cash flow is positive. The balance sheet is stronger than it has ever been. The 1 GW capacity target, while delayed, is still operationally on track.

7. Conclusion

PT Pertamina Geothermal Energy Tbk’s IPO has succeeded in its primary mandate: strengthening the company’s financial foundation through a major equity infusion while reducing its dependence on interest-bearing debt. The gross proceeds of Rp9.05 trillion have materially restructured the balance sheet, expanded shareholders’ equity to over USD 2.05 billion, and cleared the path for large-scale capacity expansion without the burden of crippling interest costs.

At the same time, the post-IPO operating record reveals real and pressing challenges. Revenue growth is accelerating — up 6.3% to USD 432.73 million in 2025 — but net income is moving in the opposite direction, declining 14.2% to USD 137.7 million as operational costs, particularly COGS, have surged nearly 20%. The USD 718.5 million cash balance, while a testament to the company’s liquidity strength, also signals that IPO capital is not yet being converted into productive energy assets at the pace prospectus-era investors expected.

From a capital market perspective, PGEO has established itself as a credible defensive ESG asset. Its stock has demonstrated resilience through geopolitical shocks, attracted analyst buy ratings with upside targets of up to 35.15%, and maintained institutional investor confidence despite the challenging 2025 earnings print.

The path forward for PGEO is clear: accelerate the conversion of idle capital into operational geothermal capacity, aggressively manage COGS through strategic global technology partnerships, and maintain the operational transparency that has begun to rebuild investor trust. With the country’s 40% share of global geothermal reserves at its disposal and the full weight of Pertamina behind it, PGEO has every structural advantage needed to fulfil its 1 GW ambition — and deliver the long-term returns its IPO investors were promised.

References

Bloomberg Technoz. (2023). Saham PGEO lesu sejak IPO, kinerja dan prospek dipertanyakan. Bloomberg Technoz.

CNBC Indonesia. (2023, March 1). IPO Pertamina Geothermal nguntungin semua pihak, ini buktinya. CNBC Indonesia.

CNBC Indonesia. (2025, June 4). Cetak kinerja solid di 2024, PGE fokus kejar target 1 GW. CNBC Indonesia.

IDN Financials. (n.d.). PT Pertamina Geothermal Energy Tbk. Retrieved from https://www.idnfinancials.com

IndoPremier. (2023). IPO PGEO justru membangun kepercayaan publik. IndoPremier.

Investor Trust. (2024). Konflik Iran tak pengaruhi kinerja Pertamina Geothermal (PGEO), saham tetap menguat. Investor Trust.

Investor Trust. (2025). Saham Pertamina Geothermal (PGEO) bisa cuan 35.15%, intip faktor pendorong ini. Investor Trust.

IPOT News. (2023). Bisnis panas bumi tinggi risiko, PGEO diminta cermat kelola dana IPO. IPOT News.

Kumparan. (2023). Anak usaha Pertamina (PGEO) resmi IPO, Wamen BUMN: Perbaiki struktur modal. Kumparan Bisnis.

PT Pertamina Geothermal Energy Tbk. (2023). Prospektus penawaran umum perdana saham PT Pertamina Geothermal Energy Tbk.

PT Pertamina Geothermal Energy Tbk. (2024). Consolidated financial statements as of December 31, 2023.

PT Pertamina Geothermal Energy Tbk. (2025). Consolidated financial statements as of December 31, 2024.

PT Pertamina Geothermal Energy Tbk. (2026). Consolidated financial statements as of December 31, 2025.

SWA. (2026). PGEO bukukan laba bersih US$137.67 juta sepanjang tahun buku 2025. SWA.

Yahoo Finance. (n.d.). PT Pertamina Geothermal Energy Tbk (PGEO.JK). Retrieved from https://finance.yahoo.com

Comments :