IPO Analysis of PT Champ Resto Indonesia Tbk (ENAK)

JIACHENG MAO

JIACHENG MAO

2702757344 · Binus Business School

IPO Analysis · Finance & Investment

PT CHAMP RESTO INDONESIA TBK (ENAK)

Initial Public Offering Analysis · February 2022

SECTION 01

Company Overview

Established in 2010, PT Champ Resto Indonesia Tbk (ENAK) is a premier Indonesian food and beverage (F&B) chain operator. The company utilises a multi-brand strategy to penetrate the rapidly expanding “modern casual dining” segment, with a complementary portfolio featuring Gokana (Japanese ramen and teppan), Raa Cha (Thai Suki and BBQ), Monsieur Spoon (French bakery and café), BMK (Indonesian cuisine), and Platinum.

ENAK’s success stems from a “pyramid” brand structure covering multi-tier consumer demands. While Gokana and Raa Cha serve as mass-market anchors providing stable cash flows, Monsieur Spoon targets the premium segment through its “French lifestyle” positioning, significantly elevating corporate image and the profit ceiling. This diversified brand matrix effectively mitigates risks from single-segment fluctuations, allowing the company to adapt to Indonesia’s rising middle class.

Unlike many competitors that rely on franchise models, ENAK adheres to a fully owner-operated model. Although asset-heavy, this ensures full terminal margins and high-precision control over service standards. Its vertically integrated supply chain — through centralised procurement and pre-processing at central kitchens — achieves significant economies of scale, lowers unit costs, and reduces waste via digital inventory management. Such absolute control constitutes ENAK’s primary competitive moat in the volatile cost environment of the post-pandemic era.

While ENAK established a profound competitive moat, its financial statements faced significant interest expense pressure during the pandemic due to heavy reliance on bank loans. This highly leveraged capital structure constrained expansion speed and posed a threat to long-term profitability. To break through this financial bottleneck and capture consumption recovery dividends post-2022, ENAK initiated its IPO — a pivotal milestone transitioning from a “purely operations-driven” to a “dual-driven” model of capital and operations.

SECTION 02

IPO Objectives & Proceeds

The primary strategic motivation for ENAK’s IPO was to achieve a fundamental transformation of its capital structure through a “Deleveraging Strategy.” Before listing, the balance sheet carried a high Debt-to-Equity Ratio (DER), restricting financing capacity and increasing default risk. By substituting debt with equity financing, the company aimed to convert high-cost term loans into permanent equity, fundamentally improving financial leverage and resilience against macroeconomic fluctuations.

At a macro-strategic level, the IPO timing aligned perfectly with the easing of COVID-19 restrictions (PPKM) in Indonesia, reflecting the urgency for expansion capital. To capture consumption rebound dividends, ENAK required capital to consolidate market leadership and secure premium locations. More importantly, expansion capital facilitated a structural upgrade of the brand portfolio — allowing strategic investment in high-growth sub-brands like Monsieur Spoon, enabling transition from mass-market dining to the premium boutique segment.

Finally, the listing was viewed as a long-term strategic investment in corporate governance and brand reputation. By listing on the IDX, ENAK committed to high standards of financial disclosure, enhancing supplier, bank, and strategic partner confidence. The listed status grants favourable bargaining power in mall lease negotiations and opens a permanent window for accessing public capital markets for future equity refinancing or M&A.

SECTION 03

Evaluation of Use of Proceeds

Approximately 56% of the funds were strategically utilised to settle outstanding loans to third parties, primarily PT Bank CIMB Niaga Tbk. Through this large-scale de-leveraging, the company significantly reduced its interest expense burden and freed up cash flow previously consumed by interest payments. In the rising global interest rate environment of 2022, this “equity-for-debt” model provided a valuable financial buffer, bringing the balance sheet to a healthy level aligned with industry benchmarks.

About 19% of the proceeds were allocated for Capital Expenditure (CAPEX) — the core engine for business growth. This encompassed new outlet openings, renovation of existing stores, and modernisation of central kitchen facilities. Particularly for Monsieur Spoon, this investment facilitated a national rollout from approximately 6 outlets in 2021 to 21 by end-2022. The total store count grew from 273 at end-2021 to 312 at end-2022, directly validating the capital deployment.

The remaining 25% was utilised for general working capital — large-scale raw material procurement, marketing campaigns, and talent acquisition. Sufficient working capital ensured supply chain stability during rapid store network expansion. With this injection, ENAK had sufficient reserves to scale inventory as the economy reopened in 2022, capturing the “revenge spending” wave and achieving a 62% revenue surge, from IDR 777 billion to IDR 1,260 billion.

SECTION 04

Post-IPO Financial Performance

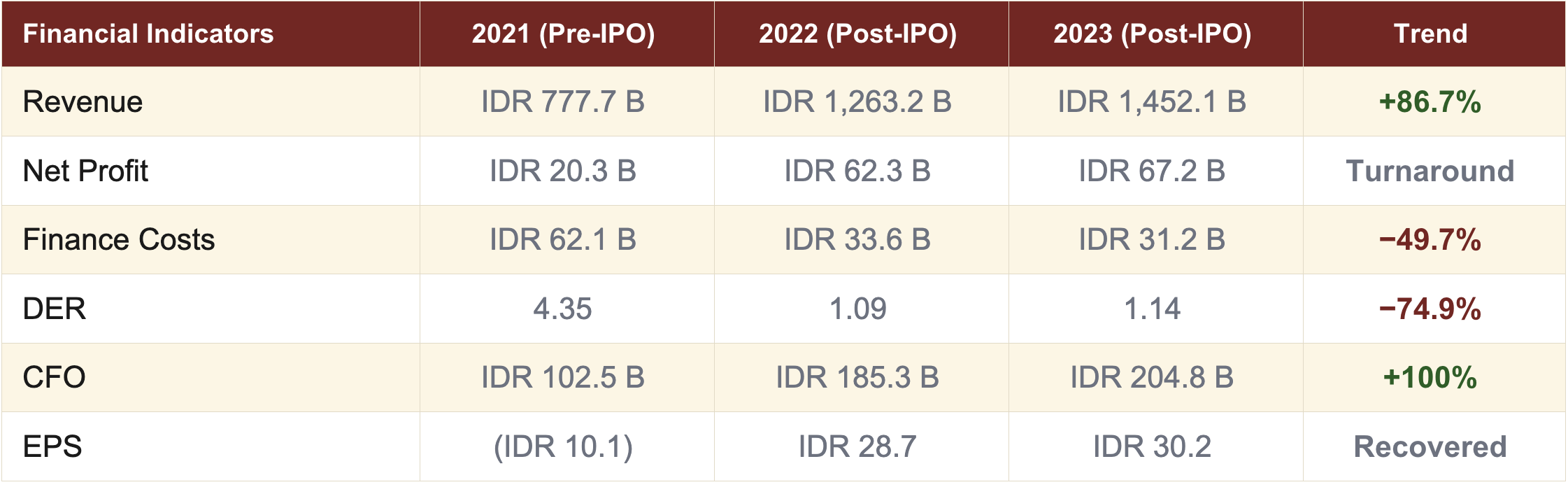

ENAK’s IPO was a highly successful case of financial and strategic transformation. Revenue surged 86.7% over two years — from IDR 777.7 billion in 2021 to IDR 1,452.1 billion in 2023. The core driver of this turnaround was not just revenue growth, but the strategic decision to prioritise debt settlement. Finance costs were slashed by approximately 49.7% within two years post-IPO, directly converting interest payments into net profit. Operating cash flow (CFO) consistently exceeded net profit, proving the strong self-generating capability of F&B operations.

The drastic improvement in the balance sheet structure is another key highlight. The DER plummeted from 4.35 in 2021 to approximately 1.0 — signalling the company’s transformation from a high-leverage entity into a financially healthy growth firm. This optimisation not only reduced financial risk but also significantly enhanced CFO quality, providing a high margin of safety for future sustained expansion.

SECTION 05

Stock Price Trend Analysis

ENAK’s stock performance since its IPO avoided the common “post-IPO dip.” On Day 1, the stock closed at IDR 945 — an 11.2% premium over the IPO price of IDR 850. The stock surged past IDR 1,200 within two months, driven by narrowing losses in FY2021 and the full recovery of mall traffic in Indonesia. By June 2022, following the release of Q1 2022 results that declared a quarterly turnaround, the stock reached its 6-month peak of approximately IDR 1,600.

Two key conclusions emerge from ENAK’s post-IPO trajectory. First, the low risk of trading below the IPO price proves that the initial pricing of IDR 850 was reasonable, offering sufficient upside for secondary market investors. Second, the high correlation between stock price and fundamentals — where the upward trajectory aligns perfectly with debt repayment and Monsieur Spoon’s expansion — demonstrates that the company is driven by growth logic rather than speculation.

Synthesising stock price, volume, and market comparisons, ENAK’s six-month post-IPO trend represents a classic fundamental-driven expansion. The market rewarded both the immediate earnings turnaround and the future expansion potential within Indonesia’s premium F&B segment. Looking ahead, ENAK’s momentum is expected to transition from “debt-reduction driven” to “organic growth driven” — with successful nationwide replication of Monsieur Spoon potentially warranting a valuation re-rating from “mass dining” to a “high-margin lifestyle brand.”

SECTION 06

Investment Decision Analysis

Synthesising the above analysis, even at the point of IPO in 2022 without knowledge of future price performance, investing in ENAK was a highly attractive and rational choice based on clear financial logic.

ENAK’s IPO demonstrated a rare combination of “high safety” and “high growth potential.” From a risk perspective, the pricing of IDR 850 provided investors with a sufficient margin of safety, backed by the tangible assets of hundreds of directly managed outlets. From a reward perspective, the allocation of 56% of proceeds to debt repayment virtually guaranteed a reduction in finance costs and a deterministic release of net profit — creating an asymmetric risk-reward profile that made ENAK a premium asset within the consumer sector.

The investment decision was supported by a powerful “dual-driver” logic: externally, it benefited from the revenge consumption rebound following the easing of COVID-19 restrictions (Macro Re-opening Play); internally, it capitalised on the rapid penetration of Monsieur Spoon into high-margin segments (Micro Brand Upgrading). This resonance between macro trends and micro execution significantly reduced investment uncertainty.

ENAK’s post-IPO stock price significantly outperformed the IHSG. Excellent trading liquidity facilitated institutional investor entry and provided market support for the stock price to stabilise above IDR 1,200 — reflecting that the market was not only paying for the immediate earnings turnaround but also re-rating the company’s long-term valuation as a leading modern casual dining platform in Indonesia. My decision: I would invest.

SECTION 07

Conclusion

ENAK’s IPO represents a textbook case of strategic capital structure transformation that successfully balanced deleveraging, expansion, and market confidence-building. By deploying 56% of proceeds toward debt repayment, the company transformed from a high-leverage entity constrained by interest costs into a financially healthy growth firm with the agility to capture post-pandemic consumption recovery dividends.

The post-IPO financial performance validated the strategy comprehensively: revenue grew 86.7% over two years, net profit recovered from near-breakeven to stable levels, and the DER plummeted from 4.35 to approximately 1.0. Operationally, the strategic investment in Monsieur Spoon proved that ENAK can successfully transition from a mass-market to a premium-segment operator — a brand evolution that could sustain long-term valuation re-rating.

The stock’s six-month trajectory — avoiding the post-IPO dip, surging to IDR 1,600, and sustaining above IDR 1,200 — is consistent with fundamental-driven appreciation rather than speculative momentum. Overall, ENAK stands as a compelling example of how a well-structured IPO, when backed by sound operational fundamentals and disciplined capital allocation, can create durable shareholder value.

REFERENCES

Sources & Bibliography

- PT Champ Resto IndonesiaTbk. (2022). LaporanTahunan 2021: Building Resilience during Recovery. Jakarta: IDX.

- PT Champ Resto IndonesiaTbk. (2023). LaporanTahunan 2022: Growth and Strategic Expansion. Jakarta: IDX.

- PT Champ Resto IndonesiaTbk. (2024). LaporanTahunan 2023: Sustainable Profitability and Brand Excellence. Jakarta: IDX.

- PT Champ Resto IndonesiaTbk. (2022).Prospektus Penawaran Umum Perdana Saham (Initial Public Offering). Jakarta: IDX.

- Otoritas Jasa Keuangan (OJK). (2023).LaporanProfil Industri Jasa Keuangan: Sektor Tbk dan Pemulihan Konsumsi. Jakarta: OJK Press.

YOUR NEXT STEP

Join MM Pro

Binus Business School

Be Part of a Global Academic Community

Sharpen your business acumen, expand your global network, and lead with confidence in the world’s most dynamic markets.

Comments :